Detroit’s bankruptcy is far and away the largest municipal bankruptcy ever. In fact, it’s more than four-times the size of the second biggest bankruptcy – the $4 billion default by Jefferson County, Alabama.

Now, most bond funds will avoid considerable losses since they’re so diversified. And many Detroit bonds were “insured” and the insurance company will cover principal losses. But that doesn’t really matter.

Detroit isn’t the reason to sell municipal bonds today. There is a far more important reason that these bonds pose a risk to your investment portfolio. Let me explain…

In yesterday’s edition of Income & Prosperity – Detroit and The Risk of Chasing Yield – I explained that investors bought Detroit bonds for the extra 2% yield.

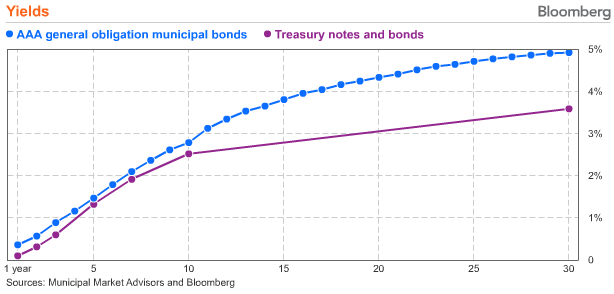

Many investors favor municipal bonds over Treasuries for the same simple reason: higher yields. The following chart shows the yield of AAA rated municipal bonds compared with U.S. Treasuries.

On top of the higher yield, municipal bonds offer the distinct advantage of being tax-free investments. This is particularly advantageous for investors in high income tax brackets. Being able to avoid federal and state income taxes can add to the already superior yield.

Now, investors in AAA rated municipal bonds face little risk of default. That’s because AAA-rated municipal bonds have the same historical likelihood of default as U.S. Treasuries at 0%.

That’s right – no municipality with AAA-rated bonds has ever gone bankrupt. Nor has the U.S. government, with its current AA+ credit rating from Standard & Poors.

But credit risk isn’t the reason to sell munis. Of course there will be more bankruptcies, some big and others small. But I’m not particularly worried about the impact of another Detroit or Jefferson County Alabama.

Instead, it’s interest rate risk that has me running away from muni bonds. And it’s a mistake for investors to focus on the Detroit bankruptcy, while overlooking this looming threat.

Long duration bonds will fall considerably if interest rates rise. And the type of bond – Treasuries, munis, or corporate – doesn’t really matter at all. In Slow Death vs. Fast Death in Bonds, I told you:

The yields on bonds are rising, and when they do, principle prices fall. As we saw recently, yields have started increasing with just a few comments from the Fed Chairman.

Consider what might happen when Bernanke raises the prime rate on Federal funds from 0.25% today to a more reasonable 1% or 2%. It could happen sooner than you might think. When that happens, the 13% losses experienced in the last two months will seem tiny.

If you own AAA rated municipal bonds, you’re earning 1% more than Treasuries. Plus, you’re getting a nice tax benefit. And you don’t even have to worry about the risk of default.

But you better be prepared for lost principal value when interest rates start rising. Even AAA bond ratings and bond insurance won’t help when the Fed starts raising rates.

The end of QE3 – also known as Fed tapering – is just the start. Looking forward a couple years, interest rates will actually start ticking up. And when they do, you won’t want to be holding Treasuries, municipal, or even corporate bonds with lengthy durations.

It’s far better to sell before this rising interest rates get underway.

P.S. Send me your thoughts on the Detroit bankruptcy. Plus, tell me how you’re protecting your investment portfolio from rising interest rates. My email address is [email protected] – I look forward to your message.