Is the classic 60/40 investment portfolio dead?

The portfolio composed of 60% U.S. stocks and 40% U.S. Treasury securities.

We answered the question last week.

And the answer was “no,” despite the portfolio posting its worst annual return last year in memory.

I am a stock picker first, and a dividend-and-income stock picker to be more precise.

If you are familiar with my Income & Prosperity articles, you know that every investment I own must cash-yield something to me.

The investment can yield 1%, it can yield 10%. But it must yield something.

That said, I’m never 100% invested.

I always maintain a reserve, usually 5% of my portfolio.

Because the reserve is a perpetual investment, I prefer that it be invested in the market instead of stored in a savings account or a money market account.

I want stock market returns combined with the lower volatility U.S. Treasury bonds provide (historically).

The classic 60/40 portfolio is a reasonable option for this constant reserve slice of my portfolio.

But return is the problem. It’s insufficient for my liking.

I have poked and prodded around for possible remedies.

I think I have found one: The classic 60/40 portfolio overlayed with a bit of leverage.

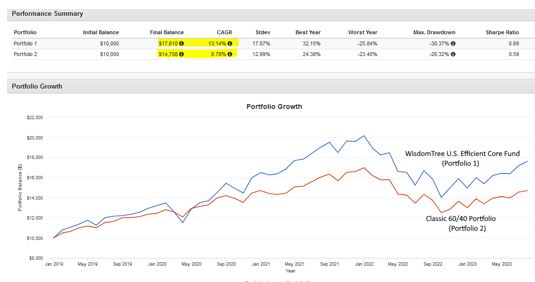

I give you the WisdomTree U.S. Efficient Core Fund (NYSEArca: NTSX).

The WisdomTree fund is a newer ETF, having launched in 2018.

WisdomTree has taken the classic 60/40 portfolio and leveraged it up to 90/60 (90% stocks and 60% U.S. Treasury securities).

The idea is that leveraging the classic 60/40 portfolio exposure to 90/60 should provide higher total returns with only marginally more risk.

Mission accomplished.

The WisdomTree ETF has averaged a 49% better average annual growth rate than the classic 60/40 portfolio – 13.1% CAGR compared to 8.8% CAGR.

What’s more, investors have had to accept only marginally more risk with the WisdomTree ETF compared to the classic 60/40 portfolio.

The worst year for performance and maximum drawdowns for the two portfolios are separated by only two percentage.

I have another option for a leveraged portfolio if you are willing to accept more risk.

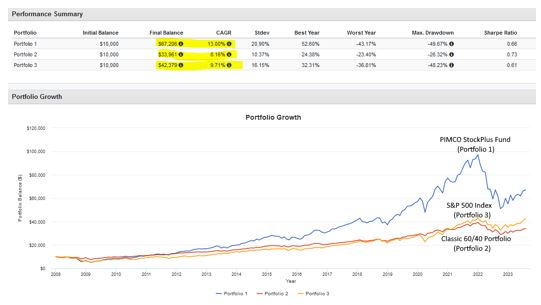

The legendary bond-investing firm PIMCO has been leveraging the classic 60/40 portfolio longer than most.

PIMCO launched its PIMCO StockPlus Long Duration Fund (PSLDX), a mutual fund, in 2007.

But instead of a 60/40 split, like the WisdomTree ETF, PIMCO goes 50/50, and then leverages the 50/50 to 100/100.

PIMCO also blends in riskier corporate bonds. Corporate bonds offer more yield than U.S. Treasury bonds, but also more credit risk.

No surprise here, the PIMCO fund is significantly more volatile than the WisdomTree ETF.

Nevertheless, the PIMCO fund’s long-term returns have been respectable, generating nearly five percentage points more CAGR than the classic 60/40 portfolio and more than three percentages CAGR than the S&P 500 over the past 15 years.

But you pay for it.

The PIMCO fund’s worst year and maximum drawdown were 20 percentage points greater than the classic 60/40 portfolio.

PIMCO’s worst years were even worse than a 100% S&P 500 stock fund.

But you were compensated with higher return.

A $10,000 investment in 2007 is double today the same investment in the S&P 500.

But as a reserve investment?

I think the WisdomTree ETF is the more appropriate fit.

Good Fortunes,

Steve Mauzy

(Disclosure: I own NTSX and PSLDX)