What’s the real effect of the Fed’s proposed “taper?”

I'm sure you noticed the hard sell in stocks that started a couple of weeks ago. In just two days, most of the major stock-market barometers were down 2.5% to 3%.

The drop in equity prices gave more than a few pundits the vapors. "Was this the end of the great four-year rally?" many gasped.

At the same time, "tapering" went viral and was soon crossing investors' lips from Tokyo to Toronto and points in between. As often happens, within a 48-hour span the word "tapering" became overworked, overused, overrated and overplayed. Such is the disseminating and repetitive nature of our modern media culture.

With that preamble, permit me to flog the word a bit on my own.

Tapering, as you now know, refers to the Federal Reserve's withdrawal from the Treasury and mortgage-backed securities (MBS) market.

A fortnight ago, investors were fearful the Fed was stealthfully reducing its monthly multi-billion dollar MBS purchases. Thus, the Fed was lowering demand for these securities, which raised their yield. The effect would cascade, and general interest rates would rise.

Equity investors were spooked by the prospect of rising interest rates lowering equity values. After all, interest rates are a discounting mechanism – the higher the rate, the lower the equity value.

But all we need to know is that higher-yield and high dividend-growth stocks tend to be less sensitive to changing interest rates than their lower-yield, low dividend-growth stock brethren.

The Fed's money creation further muddies the water. The Fed purchases MBS (or other securities) with newly minted money. Thus the Fed's unprecedented foray into money creation raises the question of what drives value. Are equity values driven by money looking for a home or by company fundamentals?

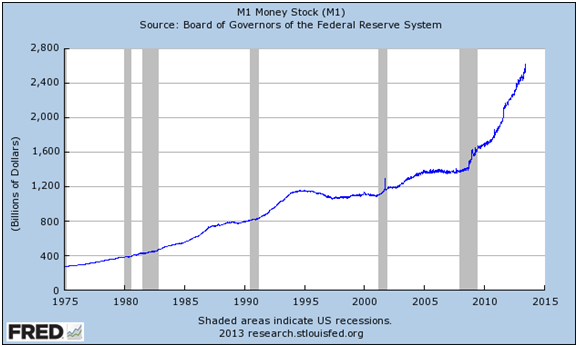

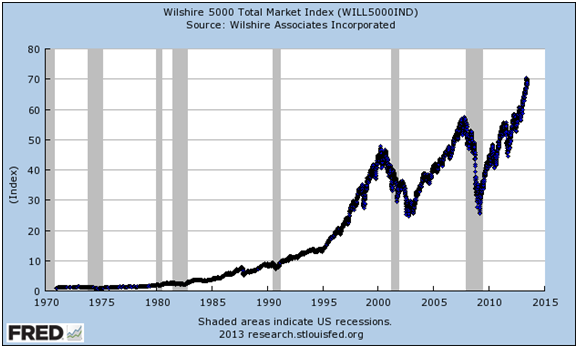

The two graphs below – one of M1 money stock, the other of the Wilshire 5000 – reflect an obvious correlation between money supply and stock prices. Both money stock and equity values are decidedly up over the past four years.

Now, I'm not saying that money stock and company fundamentals aren't mutually exclusive – it's not one or the other. Yes, fundamentals contribute to value, but fundamentals are influenced by money creation and money flow.

Consider a company with long-lived assets. If the dollar value of its revenue is rising because of increased money supply (inflation) and it doesn't need to replace assets at the rate of its money-induced revenue growth, its margins will expand. Fundamentally, the company will look better and command a high P/E multiple. But economically little has changed, except that its customers are paying more for its products in inflated dollars while the company itself has not yet entered the market to replace depreciated, worn assets by purchasing new assets with inflated dollars. (Its costs would rise when it did.)

What we have is a company with rising revenue but stable costs, which leads to widening margins.

I'll admit this is eye-glazing stuff, but it's important to understand that markets are complicated … and that what seems apparent rarely is. The point I want to emphasize is that money supply obviously matters.

And this takes us back to the Fed and tapering: Is the Fed tapering? Because if it is, then the rate of money growth will slow.

As a policy, I don't believe the Fed is tapering.

The Fed's net purchases of MBS have declined modestly over the past couple of months, but the reports I've read suggest this has more to do with lack of MBS supply than a change in Fed policy. Fewer mortgages were originated in February and March; in April and May volume picked up, so more MBS will have been formed for the Fed to purchase.

Ultimately, the Fed will need to cease propping the economy with low rates and easy money. But that's yet to occur, and I doubt it will occur this year. Many market participants have taken a similar view, which is why most major barometers have subsequently recovered.

To that, I can add that many of the High Yield Wealth recommendations have also recovered. I'm not surprised. The fundamentals remain sound, which is why I believe most recommendations still display superior risk-to-reward characteristics.

At this point, I’m both cautious and vigilant. If change is in order due to market circumstances, I’ll be sure to let you know.