Facebook (NASDAQ: FB) and Apple (NASDAQ: AAPL) are far and away the two most popular stocks in the market universe. It seems that investors can’t get enough of either.

But really, who can blame them? The general population is intimately familiar with these two companies, which certainly don’t suffer from lack of media coverage.

Nearly every person in America has seen (if not currently owns) an iMac, iPad, iPod or iPhone. Apple has completely taken over the personal handheld electronics market and changed the way we consume media.

On the other hand, Facebook boasts 190 million users in the U.S. Statistically, that means every other person you see today has a Facebook profile. That percentage will likely increase as the younger generation begins to log into Facebook.

Despite the strong public following for both companies, many people have yet to buy either of these stocks. Each company offers unique investment qualities, although Apple appears to be a better value given the current price.

Let me explain…

First, there is nothing wrong with Facebook. It’s a great company and I like their product. However, the stock is just too expensive above $30 (or even above $25 for that matter).

The shares trade at 57 times the $0.56 EPS estimate for 2012 and 47 times a forward EPS estimate of $0.68. Stocks have the ability to trade with absurd multiples like that for a time, but at some point those hefty valuation premiums need to be justified by explosive growth.

At this time I don’t think Facebook can grow at the kind of rate that a 57 or 47 P/E multiple commands. Additionally, the shares are quickly approaching their $38 IPO price – a level sellers completely rejected last month.

From both a technical and fundamental perspective, Facebook appears to have no upside. For more information on Facebook see Ian Wyatt’s “Five Reasons to Avoid Facebook”.

Meanwhile, Apple is positioned to move higher from both a technical and fundamental standpoint.

The shares trade at 12 times the 2012 EPS estimate of $46.88 and a tad under 11 times the 2013 EPS estimate. Recall that Facebook has a P/E of 57.

Apple deserves a much higher multiple considering it seems to report record financials after every quarter. Its stock could easily trade near 15.5 times 2012 EPS, which would result in a price target of $715.

Not only is Apple cheap at 12 times EPS (as much as 20% undervalued), but the company will begin to pay a dividend later this year. The dividend yield should be 2%, which is far more than most savings accounts and 10-year Treasury bonds currently pay.

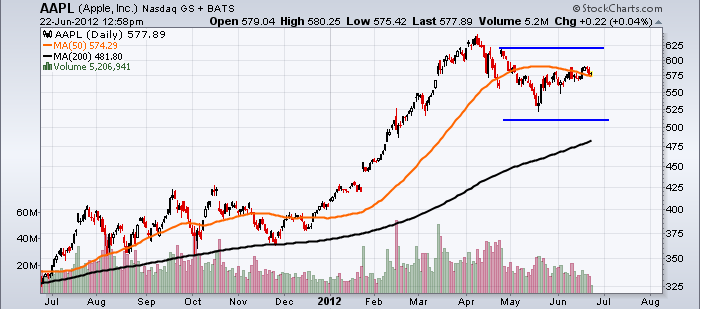

The chart also appears to favor the Apple bulls. This same chart of Apple was reviewed last month.

Fortunately, not much has changed. The $619 resistance and $510 support areas (two blue lines) are in play.

This chart shows the price of Apple shares along with an important area for you to monitor

This chart shows the price of Apple shares along with an important area for you to monitor

However, the recent selling in the broader market could result in another rapid decline in AAPL shares. The $525 zone should provide support and $510 should be an area of very strong support. If so, the downside is minimal. The lower price zone is also near the 200-day moving average (black line). Long-term investors can take a new position (or add to a current one) at any price below $545.

Traders should be ready to flip bullish should AAPL take back the 50-day moving average (orange line) near $575 and take-out $590 for a quick burst to $619. Over the much longer term, Apple should have no problem moving higher and above $700.

I could summarize this entire article in one statement. Apple has nearly endless upside due to a strong product base, and should move higher to $700 within 12 months; while Facebook shares are trapped under $38 and appears to be slowing down in its market.

Equities mentioned in this article: AAPL, FB

What’s the Best Investment: Facebook or Apple?

by Ian Wyatt